Navigating the world of credit can feel like wandering through a maze. With so many terms and numbers to understand, it’s easy to become overwhelmed. Yet, having a solid grasp on your credit report and credit score is essential for financial health in Canada. Whether you’re looking to buy a home, secure a loan, or simply want peace of mind regarding your finances, knowing where you stand is crucial.

In the vast landscape of personal finance tools available today, Borrowell™ stands out as an invaluable resource. This platform not only helps Canadians access their credit reports but also provides insights into how they can improve their scores over time. Ready to unravel the mystery behind your financial profile? Let’s dive deeper into what makes up your credit report and score and why understanding them matters more than ever.

What is a Credit Report and Credit Score?

A credit report is essentially a detailed record of your credit history. It includes information about your borrowing and repayment activities, outstanding debts, and any late payments. This document is compiled by credit bureaus and serves as a snapshot of how you’ve managed your financial obligations.

On the other hand, a credit score is a numerical representation derived from this report. Typically ranging from 300 to 900, it reflects your creditworthiness at a glance. Lenders use this score to gauge the risk associated with lending you money.

Both elements play pivotal roles in determining whether you qualify for loans or mortgages and what interest rates you’ll receive. Understanding these tools can empower you to make informed financial decisions that impact your future.

Understanding Credit Scores in Canada

Credit scores in Canada play a crucial role in your financial life. They typically range from 300 to 900, with higher scores indicating better creditworthiness.

Lenders use these scores to assess the risk of lending you money. A strong score can lead to lower interest rates and better loan terms. Conversely, a low score might result in higher costs or even denial of credit.

In Canada, two major credit bureaus—Equifax and TransUnion—calculate these scores using various data points. These include payment history, outstanding debts, length of credit history, types of credit used, and new inquiries.

Understanding how your actions impact your score is essential. Every financial decision matters—from timely bill payments to managing existing debt effectively. Stay informed about your score so you can make smarter financial choices moving forward.

Factors that Affect Credit Scores

Several factors influence your credit score, making it essential to understand them. Payment history is one of the most significant elements. Late payments can considerably lower your score.

The amount you owe also plays a crucial role. High balances on credit cards relative to their limits can signal risk to lenders. This ratio, known as credit utilization, should ideally stay below 30%.

Length of credit history matters too. A longer track record shows reliability and responsible borrowing behavior.

Types of credit accounts contribute as well. Having a mix—like installment loans and revolving debt—can enhance your profile.

Recent inquiries into your credit report can impact scores temporarily. Multiple applications for new credit in a short time may suggest financial distress or increased risk to lenders. Each element intertwines, creating the overall picture that defines your financial health.

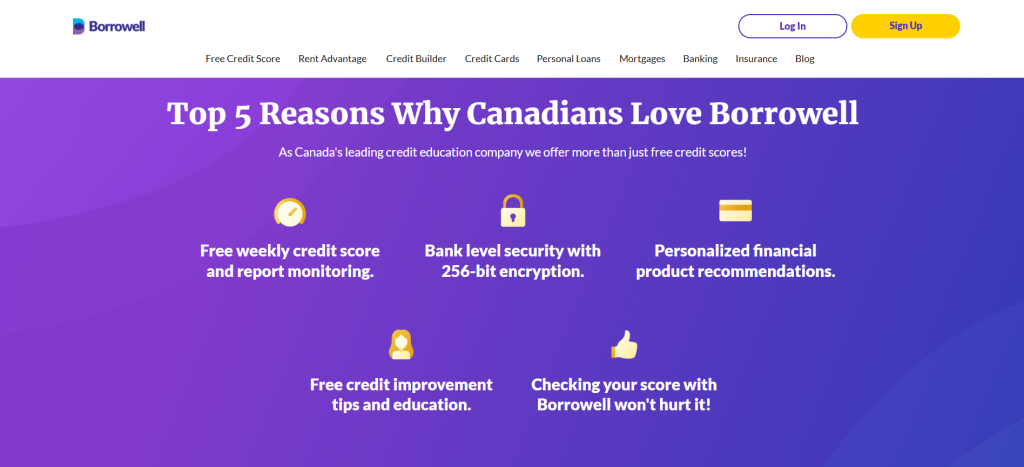

Why is it Important to Check Your Credit Report and Score?

Regularly checking your credit report and score is essential for financial health. It provides a clear picture of your borrowing history, allowing you to understand how lenders view you.

A good credit score can open doors. It increases your chances of loan approvals and helps secure better interest rates. This can save you money in the long run.

Monitoring your credit also helps identify errors or fraudulent activities early on. A simple mistake in reporting could lower your score unexpectedly, impacting future loans or mortgages.

Moreover, being aware of where you stand financially empowers you to make informed decisions. You’ll know when it’s time to improve certain areas before applying for new credit lines or big purchases.

Taking charge of this aspect of finance boosts confidence while navigating through various life stages—whether renting an apartment or buying a home.

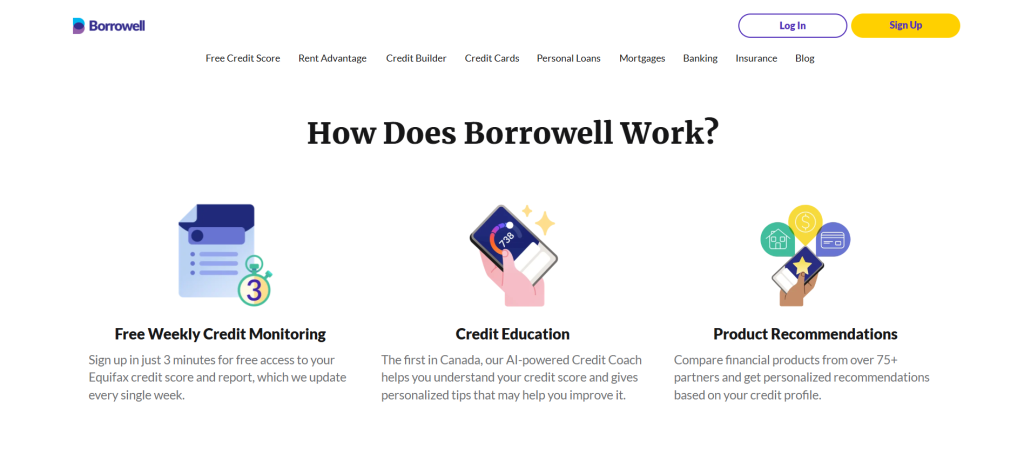

How to Get Your Free Credit Report and Score with Borrowell™

Getting your free credit report and score with Borrowell™ is simple and straightforward. Start by visiting their website, where you can create an account in just a few minutes.

Once registered, you’ll provide some basic personal information to verify your identity. This step ensures that your data remains secure while giving you access to crucial financial insights.

After verification, you’ll receive your credit report along with your credit score. It’s updated regularly, so you can track any changes over time effortlessly.

Borrowell™ also offers tools and resources to help you understand the details of your report. You’ll find tips tailored specifically for improving your financial health as well.

With this easy process, staying informed about your credit becomes a breeze!

Tips for Improving Your Credit Score

Improving your credit score is a journey, not a sprint. Start by paying bills on time. Late payments can weigh heavily on your score.

Next, keep your credit utilization low. Aim to use less than 30% of your available credit limit. This shows lenders you’re responsible with borrowing.

Regularly check your credit report for errors. Disputing inaccuracies can give an instant boost to your score if corrections are made.

Consider diversifying your credit mix as well. A mix of installment loans and revolving accounts demonstrates financial responsibility.

Limit new applications for credit cards or loans too frequently; each inquiry can cause a slight dip in your score temporarily.

Establish good habits early by maintaining long-term accounts. The age of your credit history contributes positively to how creditors view you over time.

Conclusion

Understanding your credit report and score is essential for anyone looking to make informed financial decisions in Canada. A healthy credit profile can open doors to better loan rates, secure rental agreements, and even affect job opportunities. With Borrowell™, accessing your free credit report and score has never been easier.

By familiarizing yourself with the factors that influence your credit score, you empower yourself to take actionable steps towards improvement. Regularly checking your credit allows you to catch any discrepancies early on, ensuring you’re always in control of your financial health.

Whether you’re just starting out or already managing multiple accounts, there are numerous strategies to enhance your credit standing. Being proactive about maintaining a good score will serve you well throughout life’s many adventures.

Stay informed, utilize resources like Borrowell™, and prioritize good habits when it comes to managing debt and payments. Your financial future is bright when you know where you stand with your credit report and score.